Most Are Debt-Free in Under 3 Years. Here’s What They Know That You Don’t

Over 8 million Americans have used this strategy to escape debt faster than they thought possible

The transformation journey: From financial overwhelm to debt freedom

Right now, while you’re reading this, thousands of Americans are starting a journey that will have them completely debt-free in less than three years.

Not 20 years. Not 15 years. Under three years.

Meanwhile, if you’re paying minimums on $25,000 in credit card debt, you’re looking at 23+ years of payments and over $60,000 in total costs.

Same debt. Completely different timelines.

So what do these people know that you don’t?

They discovered something most people never learn about: a structured debt settlement program that allows you to resolve your debts for a fraction of what you owe—typically 40-60% less—in a timeline you can actually see the end of.

It’s not a loan. It’s not bankruptcy. It’s not some “secret government program.”

It’s a legitimate, regulated process that over 8 million Americans have used. And most people have no idea it exists until someone tells them.

I’m telling you.

Let me show you exactly how this works, why it works, and how to know if it could work for you.

Here’s What Makes This Different From Everything Else You’ve Tried

Most debt relief programs ask you to believe in a 3-year outcome with no proof along the way. That’s a tough ask when you’re already exhausted and skeptical.

This is different.

Most people see their first debt settled within 4-6 months of starting the program.

Not years. Months.

That first settlement—often saving $5,000 to $8,000 on a single account—changes everything. It’s proof the process actually works. It gives you hope. Momentum. The energy to keep going.

Here’s what real first settlements look like:

- Credit card balance: $8,400 → Settled for $2,900 (saved $5,500)

- Medical debt: $12,300 → Settled for $4,800 (saved $7,500)

- Personal loan: $6,700 → Settled for $4,200 (saved $2,500)

These aren’t hypothetical examples. These are typical first-settlement results that happen in the first few months of enrollment.

Once you see that first account marked “SETTLED” and watch thousands of dollars in debt disappear, you know this isn’t just talk. It’s real. And it’s working.

Then the rest of your debts follow over the next 2-3 years, systematically resolved until you’re completely free.

If you’re already thinking “I need to explore this,” here’s what to do:

The first step is a free consultation where they review your specific situation—your debts, your budget, your timeline. No obligation. No fees. Just real numbers for YOUR situation.

You can keep reading to learn more about how this works (I’ll explain the full process, what to watch out for, and real stories below).

Or if you’re ready to see what this could look like for you specifically, click here to get your free savings estimate.

Either way, you’ll have the information you need to make the right decision.

Now let me show you why this works when paying minimums doesn’t…

Why Credit Card Companies Settle (And Why You’re The Only One Who Doesn’t Know)

Here’s what the credit card industry doesn’t advertise:

When debts default, banks sell them to collection agencies for as little as 4-15 cents on the dollar.

Read that again.

Your $10,000 debt? A collector buys it for $400-1,500 and then tries to collect the full $10,000 from you.

The bank has already written it off. Sold it for pennies. Moved on.

So why are you still trying to pay 100% plus interest?

Debt settlement negotiates the middle ground. Instead of the bank eventually getting 4-15 cents per dollar years from now, they accept 40-70 cents TODAY.

You save thousands. They get more than they’d get otherwise. Everyone wins.

Except they’ve never told you this was an option.

They’d rather you keep paying minimums for 20+ years, generating massive interest profits, until you eventually default anyway.

Over 8 million Americans have figured this out. They’ve used debt settlement programs to resolve their debts for a fraction of what they owed.

The credit card companies know this. The banks know this. The collection agencies definitely know this.

The only person who doesn’t know? You.

Until now. Get Started Here.

The math most people never see until it’s too late

What “Under 3 Years” Actually Looks Like Month-by-Month

Let me walk you through what most people experience in a debt settlement program:

MONTHS 1-2: Assessment & Enrollment

You have a free consultation where they analyze your complete financial picture—every debt, your income, your realistic budget. No pressure. No upfront fees. Just an honest conversation about whether this makes sense for you.

If you qualify, they create a personalized strategy. Not a template. A custom plan based on YOUR specific situation, YOUR creditors, YOUR timeline.

You make one monthly payment (typically LESS than your combined minimum payments) into a dedicated account that YOU control. Your name. Your access.

MONTHS 3-6: First Settlements Begin

This is when the magic starts.

Professional negotiators start working with your creditors. They have established relationships with major banks and collection agencies. They know what each creditor will accept.

Your first debt typically settles during this window. For many people, seeing that first $8,000 balance become $3,000 is the emotional turning point. Proof that this is real.

MONTHS 7-18: Momentum Builds

More debts settle. The pile shrinks visibly. Your stress decreases noticeably.

You’re making ONE payment instead of juggling 5-8 cards. Your phone stops ringing with collection calls. Your mail becomes boring again.

Most importantly? You can see the end. It’s not an abstract “someday.” It’s a concrete timeline you’re actively progressing through.

MONTHS 18-36: Final Settlements & Freedom

The remaining debts get resolved systematically. By month 24-36, most people are completely debt-free.

Not “paid down.” Not “refinanced.” DEBT-FREE.

The total amount paid—including all settlements and program fees—is typically 50-70% of what you originally owed.

You’ve saved tens of thousands of dollars and gained back 15-20 years of your life.

Your roadmap to debt freedom in 12-48 months

No obligation • No upfront fees • See your personalized plan

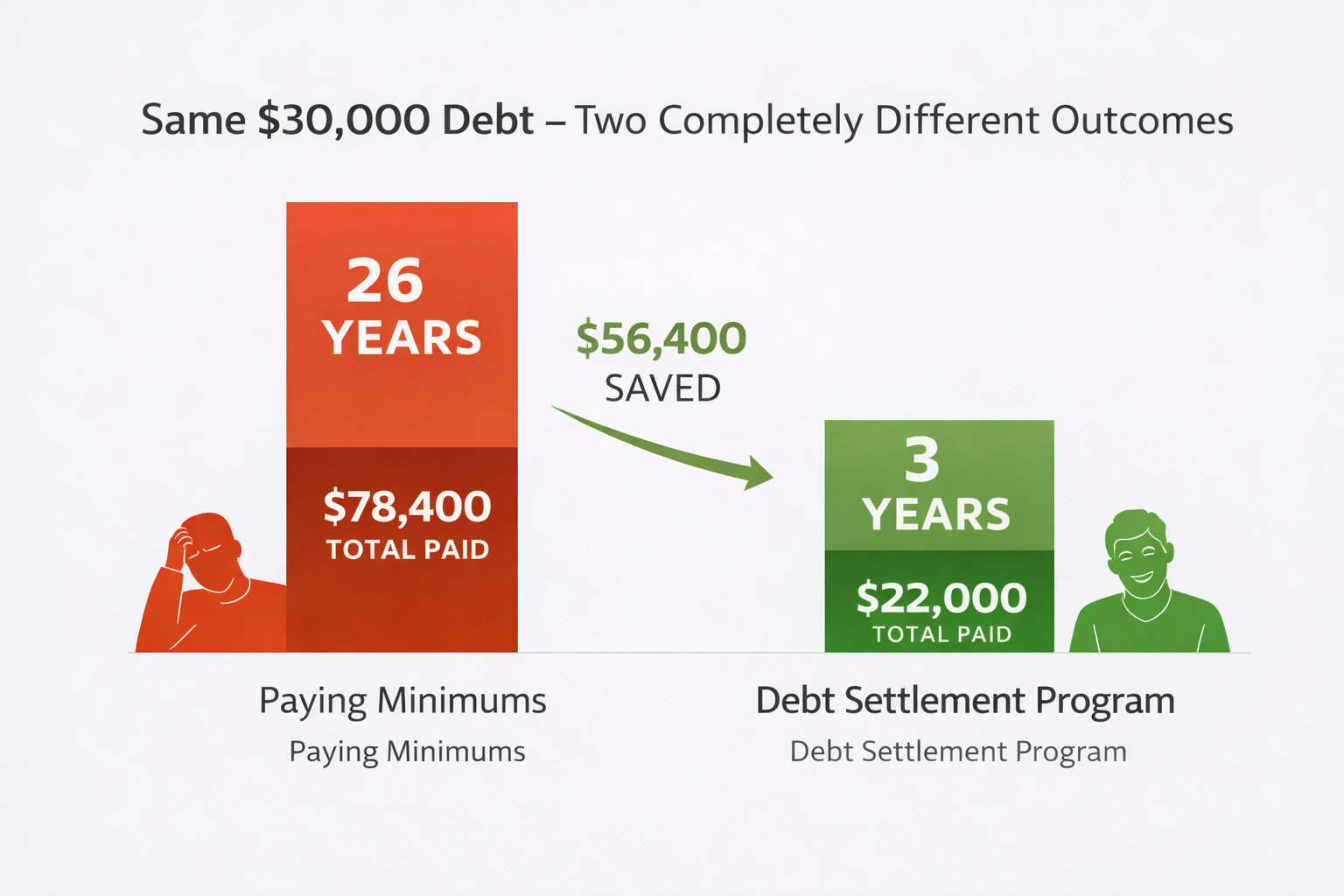

Two People, Same Debt, Completely Different Outcomes

Let me show you the real difference between the path you’re on and the path most people don’t know exists:

PERSON A: Keeps Paying Minimums

- Starting debt: $30,000 across 6 credit cards

- Monthly payment: ~$750 (minimums)

- Years to payoff: 26 years

- Total amount paid: $78,400

- Wasted on interest: $48,400

- Age when debt-free: If they start at 40, they’re 66

- Support system: None (doing it alone)

- Stress level: Constant, for decades

PERSON B: Uses Debt Settlement Program

- Starting debt: $30,000 across 6 credit cards

- Monthly payment: ~$625 (into settlement account)

- Years to payoff: 2.5-3.5 years

- Total amount paid: ~$22,000 (settlements + fees)

- Money saved: $56,400 compared to Person A

- Age when debt-free: If they start at 40, they’re 43

- Support system: Dedicated team, account manager, professional negotiators

- Stress level: High initially, decreasing monthly, gone by year 3

The difference 26 years vs 3 years makes

Same starting point. Same debt. Same basic monthly payment amount.

26 years apart at the finish line.

Person A will be making payments while their kids are in college.

Person B will be debt-free before their kids start middle school.

The only difference? Person B learned this option existed.

Is Debt Settlement Right For Your Situation?

This isn’t for everyone. Let me be straight about who this helps and who it doesn’t.

Debt settlement typically works well if you:

- Have at least $10,000 in unsecured debt (credit cards, medical bills, personal loans)

- Are struggling to make minimum payments—or already behind

- Have credit that’s already damaged from maxed-out cards or late payments

- Can’t qualify for consolidation loans (credit score too low, debt-to-income too high)

- Want to avoid bankruptcy but need a real solution

- Can commit to monthly payments of $400-800 (often less than current minimums)

This probably doesn’t make sense if you:

- Have pristine credit and can get a low-rate consolidation loan

- Owe less than $10,000 (other strategies might work better)

- Have mostly secured debt (mortgages, car loans)

- Can comfortably afford minimums and want to protect your credit score

- Are already in bankruptcy proceedings

The companies that do this well will tell you honestly if debt settlement isn’t your best option. Sometimes it’s not. Sometimes consolidation makes more sense. Sometimes even bankruptcy is the right call.

But for millions of people, debt settlement is the solution they didn’t know was available.

No obligation • No upfront fees • See your personalized plan

Let’s Talk About What This Actually Involves (The Good And The Not-So-Good)

I’m not going to blow sunshine. You deserve to know exactly what you’re getting into.

Here’s what will happen:

Your credit score will drop initially.

When you stop paying creditors directly and enter a settlement program, they report accounts as delinquent. Your score takes a hit.

But here’s the reality: if you’re already maxed out on cards or behind on payments, your score is already dropping every month. And compared to bankruptcy (which destroys credit for 7-10 years), settlement is far less damaging.

Most people’s credit starts recovering 12-18 months after program completion.

Creditors will call for a while.

During the first few months, before settlements start happening, creditors will try to contact you. It’s uncomfortable.

Reputable settlement companies help manage this. They provide you with scripts for what to say. Many offer services where they field calls on your behalf.

And honestly? Compared to 20+ years of drowning in debt, a few months of annoying phone calls is a small price to pay.

There are fees involved.

Legitimate debt settlement companies charge fees—typically 15-25% of the amount enrolled or the amount saved.

But here’s what matters: No upfront fees. They don’t get paid until your debts are actually settled.

This aligns their incentives with yours. They succeed when you succeed. If they don’t settle your debts, they don’t get paid.

Compare that to paying $48,000 in interest to credit card companies over 26 years. The settlement fees are a fraction of what you’d waste otherwise.

Not every debt may settle.

Some creditors are tougher to negotiate with. Some may threaten lawsuits (though most don’t follow through).

Good companies are upfront about this. They’ll tell you which creditors typically settle and which are more difficult. They’ll adjust strategy as needed.

The bottom line: Is it perfect? No. But compared to the alternative?

Three years of strategic discomfort versus 25 years of drowning.

Most people take the three years.

The moment it becomes real: Your first settlement confirmation

If you’re starting to see how this could work for your situation, you can see what this could look like for you with a free, no-obligation consultation. They’ll review your specific debts and give you real numbers—not generic promises.

What Separates Legitimate Programs From Predatory Ones

Not all debt settlement companies are created equal.

Some are legitimate, regulated, professional operations that have helped thousands of people.

Others are borderline scams that take your money and disappear.

Here’s how to tell the difference:

🚩 RED FLAGS (Run Away):

- Charges upfront fees before settling anything

- Promises to settle 100% of your debts guaranteed

- Pushes you to enroll immediately without reviewing your situation

- Can’t explain fees clearly or dodges questions

- No state licensing or industry accreditation

- Tells you to stop all contact with creditors without a plan

✅ GREEN FLAGS (Legitimate Companies):

- No upfront fees – Only charges after debts are settled

- Transparent pricing – Explains all fees clearly before enrollment

- Free consultation – Reviews your situation with no obligation

- Realistic expectations – Tells you this takes 2-4 years, acknowledges credit impact

- Personalized strategy – Customizes plan to your specific debts and budget

- Industry credentials – Licensed by state, member of AFCC or AADR

- Dedicated support – Assigned account manager, not a rotating call center

- Clear process – Explains exactly how your money is held and how settlements work

The companies worth working with:

- Have helped thousands of clients successfully

- Are regulated by the FTC and state agencies

- Put your money in accounts YOU control

- Let YOU approve every settlement before it’s finalized

- Provide regular updates and transparent progress tracking

- Admit when debt settlement isn’t the best option for someone

These companies exist. They do this work professionally and ethically.

Your job is to find them and avoid the predators.

Why People Hire Professionals Instead of Negotiating Alone

You might be thinking: “Can’t I just call my creditors and negotiate myself?”

Technically, yes. Some people do.

But here’s why most don’t succeed:

1. Creditors know you don’t know what you’re doing.

They have professional collectors who negotiate for a living. You’re calling once, stressed, desperate. They smell it. They’ll offer you a payment plan at full balance instead of settlement.

Professional negotiators have relationships with these companies. They know what each creditor actually accepts. They know the right language, the right timing, the right leverage points.

2. You need multiple debts settled, not just one.

Getting one creditor to settle? Maybe doable.

Coordinating settlements across 5-8 creditors, timing them strategically so you don’t run out of funds, knowing which to approach first, managing the legal risks? That’s exponentially harder.

3. Emotional exhaustion is real.

When you’re drowning in debt, you’re already mentally drained. The idea of calling creditors, getting rejected, trying again, tracking everything, managing the stress—most people can’t sustain that for 2-3 years.

Having a team that handles negotiations while you just make one monthly payment? That’s worth the fees for most people.

4. Legal protection.

If a creditor sues you during the process (uncommon but possible), professional settlement companies have legal resources and protocols. They know how to respond, which attorneys to connect you with, how to protect you.

On your own? You’re Googling “what to do when sued for credit card debt” at 2am.

5. Structured savings discipline.

The program requires you to deposit monthly into a dedicated settlement account. That forced structure keeps you on track.

Without it, many people spend the money on emergencies and never accumulate enough to settle anything.

Can you do it yourself? Maybe.

Will you actually succeed doing it alone over 2-3 years? Most people don’t.

That’s why debt settlement companies exist. They provide structure, expertise, emotional support, and systematic execution that most individuals can’t maintain on their own.

What People Actually Experience (In Their Own Words)

Let me share what this journey looks like for real people:

Sarah, 44, Phoenix – $34,200 in Credit Card Debt

“I was paying $850 a month in minimums and the balance barely moved. I felt like I was running on a treadmill forever. My husband and I fought constantly about money.

The first settlement happened in month 5—a $9,200 card settled for $3,800. I literally cried when I got the confirmation letter. It was the first time in years I felt like there was actual hope.

29 months later, we were completely debt-free. We paid about $21,000 total instead of the $34,000 we owed. More importantly, we got our marriage back. We sleep at night now.

I wish I’d known about this five years earlier. I wasted so much time paying minimums.”

Marcus, 51, Atlanta – $28,900 in Medical and Credit Card Debt

“After my wife’s surgery, we had $18,000 in medical bills on top of existing credit card debt. I’m a teacher—I don’t make enough to handle $1,100 a month in debt payments.

I was skeptical at first. It sounded too good to be true. But the consultation was free and the guy was honest about what to expect, including that my credit would take a hit.

Here’s what sold me: He said ‘Your credit is already damaged from maxed cards. This gives you a path to recovery instead of drowning for 20 years.’

First debt settled in 4 months. Total program took 26 months. My credit actually started improving about a year after I finished because I had no debt and was building positive history.

Best decision I made. I’m 51—I didn’t have 20 years to waste on minimum payments.”

The Rodriguez Family, Dallas – $51,000 Combined Debt

“We’re immigrants. We built our credit from scratch, then life happened—job loss, medical emergency, poor decisions trying to stay afloat.

We were embarrassed. In our culture, you don’t talk about debt. You definitely don’t ‘settle’ it—you pay what you owe.

But we did the math. At minimums, we’d be paying until our kids were in college. We’d never save for their education. Never buy a house. Never retire.

The company we worked with had Spanish-speaking staff who understood our situation. They didn’t judge. They just helped us make a plan.

42 months later—debt-free. We paid about $33,000 instead of $51,000. More importantly, we could start saving for our kids’ future.

We learned: Being smart isn’t the same as being dishonorable. Taking care of your family’s future is the honorable choice.”

These aren’t paid testimonials. These are the stories you hear when you ask people who’ve actually done this.

The common themes?

- Relief after the first settlement (proof it works)

- Regret they didn’t know about it sooner

- Surprise that it actually worked as promised

- Life transformation beyond just money (relationships, sleep, hope)

Life after debt: Planning for the future instead of surviving the present

Here’s What Happens Next (And What Doesn’t)

You have three options right now:

Option 1: Keep doing what you’re doing.

Keep paying minimums. Keep watching the balance barely move. Keep fighting with your spouse about money. Keep avoiding your mailbox. Keep waking up at 3am doing math in your head.

In 5 years, you’ll be in roughly the same position—just older, more exhausted, and deeper in interest payments.

Option 2: Do nothing and hope it gets better.

Hope for a windfall. Hope the debt somehow resolves itself. Hope your income doubles.

How’s that been working so far?

Option 3: Get information.

Have a free consultation. Learn your actual options. See real numbers for your specific situation. Decide based on facts instead of fear.

Here’s what the consultation actually involves:

- 20-30 minute phone call (not hours of your time)

- They review your debts, income, and monthly budget

- They tell you honestly if debt settlement makes sense for you

- If you qualify, they show you a personalized plan with real numbers

- You get to ask every question you have

- Then YOU decide. No pressure. No obligation. No upfront fees.

What it doesn’t involve:

- No hard sell or pressure tactics

- No obligation to enroll

- No fees for the consultation

- No judgment about how you got here

The worst that happens? You spend 20 minutes on a call and learn it’s not right for you. You’re back where you started, just with more information.

The best that happens? You discover a path to being debt-free in under 3 years instead of 20+ years. You save tens of thousands of dollars. You get your life back.

No obligation • No upfront fees • See your personalized plan

Why “I’ll Think About It” Usually Means “I’ll Keep Suffering”

I need to be honest with you about something:

Most people who read this article and think “That’s interesting, maybe someday” never follow up.

Not because they don’t need help. They desperately do.

But because debt has a way of paralyzing decision-making. The shame, the overwhelm, the exhaustion—it all creates inertia.

Here’s what typically happens:

- You bookmark this article

- You tell yourself you’ll look into it next month

- Next month comes and you’re dealing with another crisis

- Six months pass

- You’ve paid another $3,000-4,000 in minimum payments

- $2,500 of that was pure interest that bought you nothing

- You’re no closer to freedom

- Now you’re six months older and $2,500 deeper in wasted payments

And the whole cycle repeats.

Meanwhile, someone else who read this article today:

- Made the call

- Had the consultation

- Enrolled in a program

- Six months from now, they’ll have their first debt settled

- They’ll be on a concrete path to freedom

- They’ll sleep better

- Their relationships will improve

- They’ll have hope

Same starting point. Different decision. Completely different life trajectory.

The consultation is free. It costs you nothing but 20 minutes.

You’ve spent more time than that scrolling social media today.

What’s really stopping you?

If it’s fear of being judged: The people who do this for a living have seen everything. They don’t judge. They help.

If it’s skepticism: Good. Be skeptical. Ask hard questions in the consultation. Get facts, not promises.

If it’s shame: Everyone in debt feels shame. Everyone. But staying in debt because you’re ashamed doesn’t help anyone.

If it’s “I should be able to handle this myself”: You’ve been trying. For how long? Has it worked?

Eight million Americans have used debt settlement programs.

They’re not weak. They’re not failures. They’re smart enough to recognize when they need help and brave enough to ask for it.

The only question that matters:

Do you want to be debt-free in 3 years or still struggling in 20?

The free consultation: Just a conversation about your options

Take The First Step: Free Consultation, No Obligation

Here’s exactly what to do next:

Click the button below to access a free, no-obligation consultation.

You’ll provide some basic information about your debt situation (how much you owe, types of debt, monthly income). This takes about 3-4 minutes.

Then you’ll schedule a call with a debt specialist at a time that works for you—evenings and weekends available.

On that call, they’ll:

- Review your specific financial situation

- Tell you honestly if debt settlement makes sense

- Show you a personalized plan with real numbers

- Explain the process, timeline, and fees clearly

- Answer every question you have

What they won’t do:

- Pressure you to enroll

- Charge you anything for the consultation

- Judge you for your situation

After the call, you decide. That’s it.

If debt settlement makes sense, you move forward.

If it doesn’t, at least you know. You have information instead of questions.

No obligation • No upfront fees • Personalized to your situation

The Choice Is Yours

Two paths.

Path 1: Keep paying minimums. Twenty-three more years. $48,000 in interest. Constant stress. Postponed dreams.

Path 2: Debt settlement program. Under 3 years. Save $20,000-40,000. Systematic path to freedom.

Thousands of people choose Path 2 every single day.

Not because they’re giving up. Because they’re being strategic.

Not because they’re irresponsible. Because they’re choosing their family’s future over a bank’s profit margin.

The credit card companies already know about debt settlement. They factor it into their business models. They expect it. They accept it.

The only person who doesn’t know about it is you.

Now you know.

What you do with that information is up to you.

12-48 months from now, you’ll be either:

A) Debt-free, building savings, sleeping through the night, planning for your future

OR

B) Reading another article like this, still stuck, still struggling, still hoping something changes

Don’t be Person B.

Make the call.

The consultation is free. The information is free. What you do with it is your choice.

But at least know what’s possible.

No obligation • No upfront fees • Pay up to 50% less than you owe